Blog Post

How Do Non-profit Hospitals Give Back?

A breakdown of community benefit spending

Hospitals designated as non-profits received tax-benefits valued at over $24 billion annually in 2011. Non-profit hospitals justify their tax-exempt status by providing “community benefits” in the form of free and subsidized care, investments in public health, and community-based initiatives intended to address the social determinants of health, such as food or housing insecurity. Whether non-profit hospitals truly benefit their communities has been dogged by controversy and calls for reform. Many observers assert that hospitals avoid making sustained community investments in favor of counting millions of dollars of “discounts” to low-income patients as community benefits while aggressively pursuing unpaid bills.

Two recent papers by LDI Senior Fellows Krisda Chaiyachati and Rachel Werner provide new data to inform the debate: detailed estimates of how much hospitals spend on different types of community benefits, whether community benefits are matched to local need, and what effects community benefits have on health outcomes.

Chaiyachati and Werner analyzed Internal Revenue Service (IRS) tax data from over 1,600 non-profit hospitals. By law, hospitals report total spending on community benefits, broken out by health care-related spending (e.g., free care), community-directed spending (e.g. anti-smoking initiatives or funds for local community organizations), and research and educational activities. To standardize comparisons, the authors measured all spending as shares of total hospital expenditures.

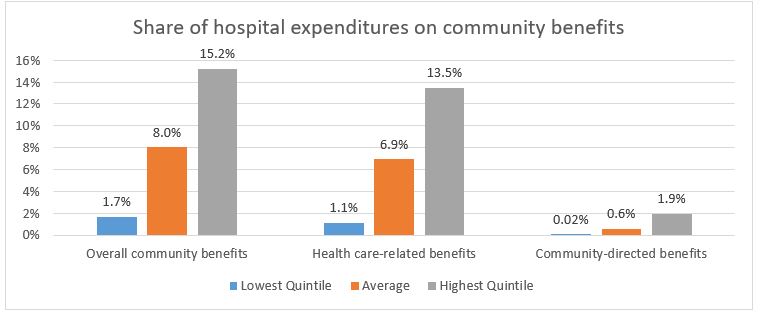

The results suggest that hospitals still rely on discounted charity care to meet community benefits requirements. In 2014, non-profit hospitals reported that they spent an average of 8.1% ($17 million) of their total expenditures on community benefits, more than 80% of which was health care-related. On average, 6.7% ($11 million) of expenditures were on health care services, compared to 0.7% ($1.2 million) for community-directed contributions. The remainder of community benefits were on educational and research initiatives, which the authors did not analyze specifically.

Diving deeper, spending seems unrelated to local needs, which the authors measured using ZIP code level demographic and socioeconomic data. While communities with higher Hispanic, unemployed, and uninsured populations had higher total community benefit spending, the effect was driven by higher health care-related spending, such as discounted or free care, rather than community-directed contributions. No measure of local socioeconomic deprivation was associated with higher spending on community-directed initiatives. For example, hospitals in ZIP codes with the highest poverty rates spent no more on community-directed benefits than hospitals in affluent ZIP codes.

The authors then analyzed each socioeconomic characteristic separately, controlling for hospital characteristics (e.g. church-affiliation and teaching status), community characteristics (e.g. rural versus urban), and level of market concentration. With those controls, no measure of poverty or social need was associated with increased total community benefits, health care-related benefits, or community-directed spending.

The results are disappointing in light of a second study from Werner and Chaiyachati, which suggests that community-directed spending could improve health outcomes, specifically, 30-day readmission rates. Readmissions rates are a useful measure of health care quality—capturing in-hospital care, discharge planning, and follow-up. Since the Affordable Care Act, hospitals have been financially penalized for high readmission rates. Critics, however, argue that hospitals cannot control social forces that lead to high readmission rates. In theory, non-profit hospitals can achieve two goals with community-directed spending: reduce readmissions rates that lead to financial penalties and meet IRS community benefit requirements.

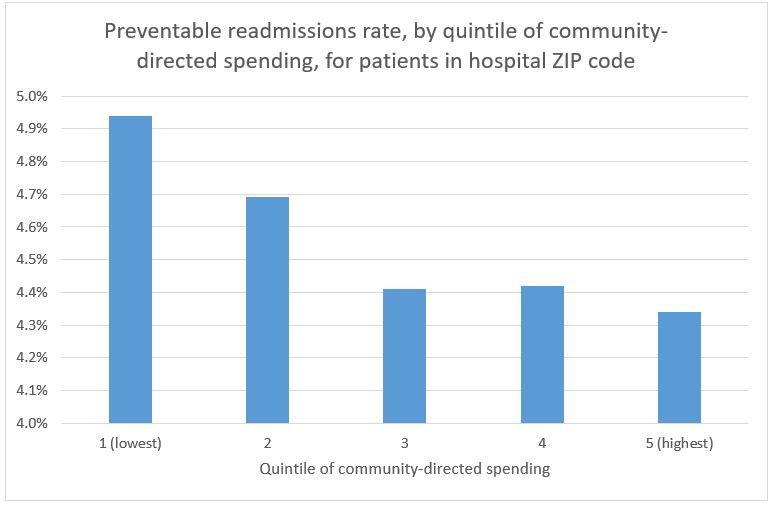

That sounds great in theory, but does community-directed spending actually lead to fewer avoidable readmissions? Werner and Chaiyachati assessed whether community benefit expenditures were associated with 30-day readmissions rates for Medicare patients at 1,405 non-profit hospitals. After controlling for patient health and socioeconomic factors and hospital characteristics, hospitals with the highest levels of community-directed expenditures had significantly lower rates of readmissions. Medicare patients at hospitals in the highest quintile of community-directed spending had a readmissions rate of 15.3%, compared to 16.5% at hospitals in the lowest quintile of community-directed benefits—an absolute difference of 1.2% and relative difference of 7.3% fewer readmissions. The authors found no relationship between readmission rates and overall or health care-related community benefits spending, such as discounted or free care.

The magnitude of the reduction in readmissions rates was highest for patients living in the same ZIP code as the hospital—suggesting a hyperlocal effect. Furthermore, the relative decline in readmissions was larger among preventable readmissions, which are most sensitive to social needs, compared to all-cause readmissions. Taken together, the evidence suggests that increased investment in the social determinants of health, rather than simply writing off free care, has a significant impact on measurable health outcomes.

So, why haven’t hospitals increased community-directed spending? One hypothesis is that free care is easier to implement, while community-directed spending requires creativity, and until now, the financial case hasn’t been clear. Now, the evidence is in: a little bit goes a long way. In their study of readmission rates, Werner and Chaiyachati found that, on average, 0.6% of expenditures ($1 million) were on community-directed benefits, and the highest quintile of community-directed spending was 1.9% of expenditures. Put another way, the gap between least and most generous hospitals is relatively narrow. Most hospitals can make strides at relatively low cost.

Oversight of community benefits has come a long way. Historically, vague legislation and lax regulation allowed hospitals to write off the revenue shortfall between public programs (i.e., Medicaid) and private insurance as a community benefit. In 2008, the IRS required hospitals to provide more detailed reports on Schedule H forms, differentiating between levels of free or subsidized care, investments within the community, and educational and research activities. Beginning in 2012, the Affordable Care Act required that hospitals conduct and report Community Health Needs Assessments (CHNA) to identify local needs in collaboration with public health and community leaders.

Schedule H forms have enabled new research into the community benefits program, infused the debate with much-needed data, made it possible to track changes over time, and allowed more detailed analyses of the value of different types of community benefits. Without prior efforts to reform community benefits, it would be impossible to make the case that hospitals can and ought to do more.

Further reform in the tax code or through legislative action may be needed to target community benefits more effectively. But in a sense, this is a story of iterative policy at work. For non-profit hospitals, a growing evidence base suggests that investing in communities’ social needs is an effective way of fulfilling their mission and a sound financial strategy.