Finding Rare Agreement on Fixing the Health Care Affordability Crisis

Former Obama and Trump Advisors Find Some Common Ground at D.C. University of Pennsylvania Event

Health Care Payment and Financing

Blog Post

Medicare has a gaming problem. The Centers for Medicare and Medicaid Services (CMS) uses an imprecise method to compensate insurers and health organizations for higher-cost patients. Gaps between expected and actual costs create opportunities to game the system for greater reimbursements, particularly through Medicare Advantage. In the next decade, these overpayments could cost $1.2 trillion.

To avoid this waste of taxpayer funds, LDI Senior Fellows Ezekiel Emanuel, Amol Navathe, and colleagues built Franklin, an artificial intelligence (AI) model, to replace Hierarchical Condition Category coding. HCC is Medicare’s current system for adjusting payments based on patients’ risk.

“Franklin is three times more accurate than HCC,” Emanuel said, when directly compared for predicting one-year care costs using claims data. “CMS could use it today to reduce overpayment.”

Franklin was designed to use the same data as HCC: diagnosis codes from traditional fee-for-service Medicare claims. This choice brings inherent limitations, said Daniel Shenfeld, the first author of the Franklin study. Traditional Medicare claims may not accurately reflect Medicare Advantage costs and patterns of care, and diagnosis codes alone are poor predictors of the highest-cost events such as hospitalizations. Nonetheless, Franklin excels at identifying lower-cost groups that are the main source of overpayments.

HCCs are diagnostic code groups for expensive conditions, such as heart disease, asthma, or cancer. CMS applies HCCs to the previous year’s traditional Medicare claims data to set new payment adjustments for patients with specific health risks. In 2024, CMS used HCC to partially or fully risk-adjust payments for 65 million Medicare Advantage or Obamacare marketplace enrollees or patients in Accountable Care Organizations.

Risk adjustment intends to reward efficient care. If treatment costs less than expected, insurers and health systems keep the difference. However, this arrangement facilitates “upcoding,” meaning adding more – or more severe – codes to medical records. It also encourages favorable selection, meaning designing plans and targeting marketing to enroll beneficiaries whose costs are lower than predicted.

Improving risk-adjustment accuracy could reduce this behavior, said Shenfeld, a Penn health policy adjunct professor and founder of Manganese Health, a health technology consultancy. A risk-adjustment model that more precisely predicts true costs reduces incentives to exploit CMS for financial gain, but with the tradeoff of lowering the incentive for efficient care.

To build Franklin as a plug-and-play HCC replacement, the team used machine learning, a type of AI that can identify complex relationships among diverse data, such as age, sex, and diagnostic codes in medical claims. Franklin was trained to identify code-cost relationships using a 20% sample of 2018 traditional Medicare claims — the same data source used for the current HCC model. When Franklin’s predictions were stable and clinically sensible, Franklin and HCC competed head-to-head for predicting actual costs using 2019 claims data.

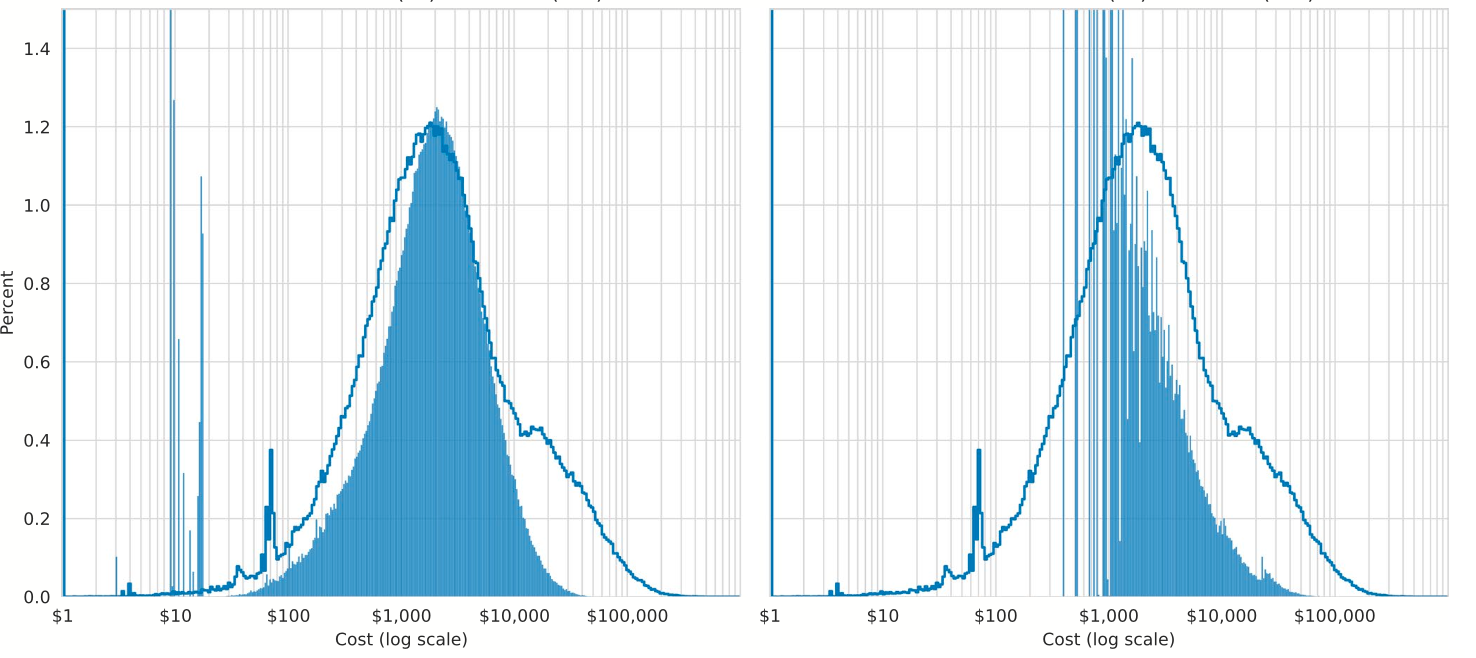

In addition to threefold higher accuracy than HCC at predicting Medicare costs overall (Franklin 0.44 vs. HCC 0.15 for R-squared, measuring fit between predictions and costs), Franklin’s predictions were significantly better across cost distributions (Figure), including at the lower end, where most overpayments arise. Testing with 2022-23 data confirmed Franklin’s superior accuracy.

Franklin better predicted costs for women, people with disabilities, rural residents, and white, Black, and Hispanic racial and ethnic groups. Franklin more often assigned Black and Hispanic beneficiaries in lower-cost categories, reflecting access inequities, the authors said. A full understanding of inequities requires additional analyses, including with claims for people dually eligible for Medicare and Medicaid. The authors note, however, the challenges of using race and ethnicity data, which are not uniformly collected across health systems.

Simulation studies showed that applying Franklin to Medicare Advantage risk adjustment could potentially reduce overpayments by $750 million to $3.25 billion annually.

By reducing discrepancies between risk-adjusted payments and actual costs, Franklin would reduce gains from upcoding and favorable selection, ensuring proper reimbursement for care. Here’s how:

Franklin is an AI model, so is “hallucination” a concern? Only generative AI models create fanciful answers, Shenfeld said. Franklin is a predictive model and the accuracy of its annual cost estimates is checked with measures such as R-squared.

Franklin is only one step toward reducing CMS overpayments, Shenfeld said, and is not totally immune to gaming. “The CMS-insurer arms race is a real concern, especially in the age of AI.” Protecting CMS requires more than a new risk-adjustment model, like ways to detect and respond to upcoding. The Franklin team, Shenfeld said, is preparing the “technological scaffolding,” like software and analytic infrastructure to implement Franklin into CMS, as part of long-term work toward a more financially efficient Medicare.

“The issue of overpayment is bipartisan, not political,” Emanuel said. “This administration has shown that it’s willing to go ahead and just do things. We have a better model, so they’d have to have a pretty damn good reason not to implement it.”

The study, “A Machine Learning Model to Improve Risk Adjustment Accuracy in Medicare,” was published on March 5, 2026 in Health Services Research. Authors include Daniel K. Shenfeld, Lindsay Warrenburg, Eli Silvert, Matthew Guido, Maggie Makar, Karen Joynt Maddox, Amol Navathe, Ravi Bharat Parikh, and Ezekiel J. Emanuel.

Former Obama and Trump Advisors Find Some Common Ground at D.C. University of Pennsylvania Event

Penn LDI Panel Cites Costs for Enrollees Alongside Billions in Overpayments and Systemic Gaming

For-Profit Hospitals Saw the Largest ER Gains, With Smaller Effects at Nonprofits

Health Insurer Acquisition of PBMs — the Prescription Drug Middlemen — Raised Premiums for Some Part D Beneficiaries

Mergers Change Where Low-Income Women Give Birth—Prompting Calls for Regulators to Weigh Effects on Vulnerable Patients and Safety-Net Systems

Former CMMI Leader Liz Fowler Cites Rigid Federal Scoring Rules and Bureaucratic Impatience for Pilot Failures